As shortly as they rose to prominence through the pandemic, many biotechs fell simply as quickly again all the way down to earth.

When pharma’s R&D push peaked, lots of of vaccines and coverings have been in improvement to fight the novel coronavirus. And whereas the remobilization turned once-obscure biotechs like Moderna into family names, a number of different corporations that had immediately emerged into the highlight finally light as their candidates faltered.

In a journey that mirrored that of the broader biotech world, the preliminary “sugar excessive” of funding {dollars} led to a crash for many corporations as capital drained from the market. Within the wake of that reckoning, many biotechs have needed to restructure in a tighter monetary market and pivot to various areas of potential progress.

Right here’s the place 4 biotechs have landed since their preliminary ascent to COVID fame.

CureVac

The backstory: When the pandemic started, Germany-based CureVac had already been plugging away at mRNA know-how. The truth is, CureVac, which launched in 2000, claims to be “the world’s first” to “harness mRNA for medical functions.” As such, the corporate was poised to change into a key participant within the COVID vaccine race, and by June 2020, it headed into part 1 trials with its candidate CVnCoV.

Regardless of early-stage outcomes that appeared encouraging, CureVac reported efficacy round 47% in a part 2b/3 trial — far under its mRNA rivals — and improvement was dropped. Many scientists initially expressed dismay at CureVac’s medical stumble. However the mismatched outcomes in comparison with different mRNA photographs was finally blamed on CureVac’s use of unmodified mRNA (versus the modified mRNA within the photographs developed by Pfizer/BioNTech and Moderna), which CureVac’s CEO Alexander Zehnder mentioned would doubtless work higher in therapeutic areas like most cancers.

The place they’re now: CureVac was down however not out. After its COVID setback, the corporate re-evaluated its mRNA know-how, established a restructuring plan and appeared to construct on its pandemic-era classes.

Earlier this yr, CureVac restructured a take care of vaccine heavyweight GSK initially struck in 2020 to bolster improvement of the pharma large’s infectious disease-focused pipeline. The partnership gave GSK full improvement and commercialization rights to CureVac’s COVID and seasonal flu candidates in part 2 and an avian influenza shot in part 1 for over $1.5 billion in upfront and potential milestone funds.

In its third-quarter earnings report launched this week, the corporate mentioned its “company redesign,” which features a 30% workforce discount, is about to ship “vital annual value financial savings” subsequent yr. Like Moderna, CureVac can be aiming to leverage mRNA in most cancers and is in early-stage improvement of personalised and off-the-shelf most cancers vaccines.

Novavax

The backstory: Like CureVac, Novavax was an early and powerful COVID vaccine contender. After just a few medical setbacks, Novavax finally scored an FDA nod for its shot in 2022. However regardless of the Novavax jab providing a conventional protein-based choice to mRNA-shy sufferers and research suggesting it might have fewer negative effects and longer sturdiness, the corporate has struggled with uptake.

Commercialization challenges hit a fever pitch earlier this yr when activist investor Shah Capital publicly known as out the financially fledgling firm for “colossal market failures” and demanded a management “shakeup.”

Weeks later, Sanofi prolonged Novavax a lifeline via a partnership to commercialize its COVID shot and co-develop its combo flu/COVID candidate.

The place they’re now: The Sanofi tie-up in Could funneled $500 million into Novavax’s R&D coffers and could possibly be value as much as $700 million extra if it delivers on improvement and regulatory milestones. To date, the highway to hitting these targets has been rocky.

In October, the FDA slapped a medical maintain on a trial of its flu/COVID shot after a “severe antagonistic occasion of motor neuropathy.” The corporate was OK’d to resume testing earlier this week.

In its newest earnings report, Novavax additionally lowered its full-year steering from a excessive of $800 million in income to $700 million on the prime quality. The corporate, which slashed R&D investments and its employees to chop prices, additionally mentioned it inked an settlement with a “main pharmaceutical firm” associated to its proprietary Matrix-M adjuvant.

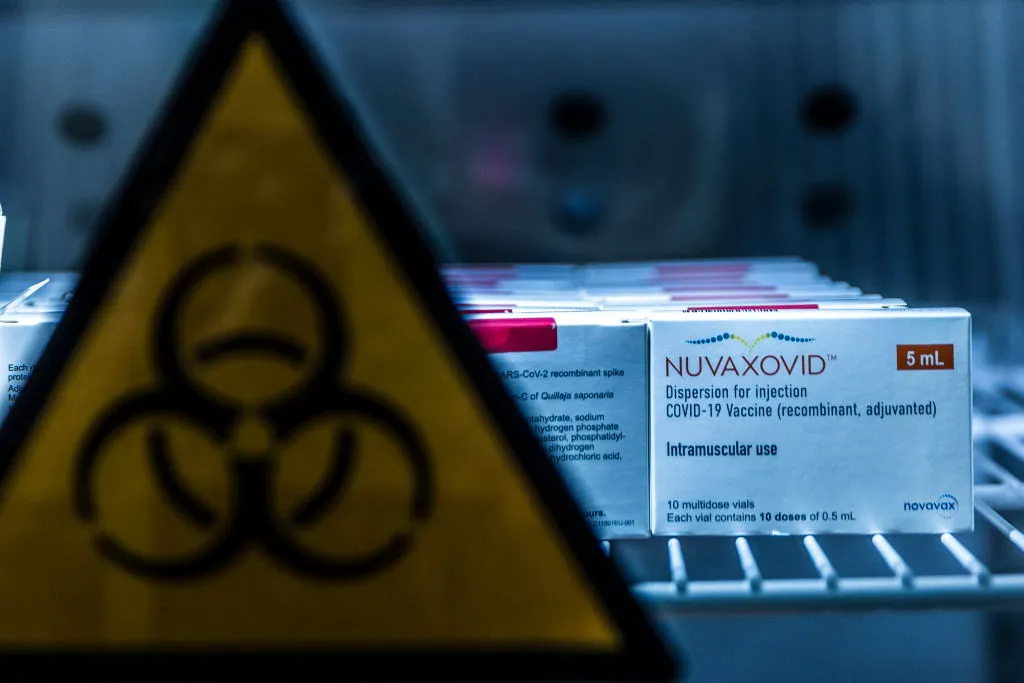

Ampoules of the COVID-19 Nuvaxovid vaccine by Novavax are saved in Berlin, Germany.

Carsten Koall through Getty Photos

Inovio Prescription drugs

The backstory: Whereas Inovio Prescription drugs was as soon as a promising frontrunner within the COVID vaccine hunt with its DNA-based know-how, the corporate additionally grew to become shortly mired in controversy.

A decade earlier, Inovio had been creating an H1N1 shot and in later years reported optimistic medical outcomes for malaria and Zika vaccines. Whereas this progress maintained monetary momentum for its medical work, Inovio did not carry a product to market.

By August 2020, the corporate gave the impression to be repeating that sample, and a bunch of shareholders filed a class motion swimsuit towards Inovio claiming it launched deceptive statements concerning the COVID vaccine to bolster inventory costs.

By 2022, the corporate gave up on its COVID shot, which might have required a specialised gadget for administration, and pivoted to creating the candidate as a booster as an alternative.

Final yr, Inovio settled the category motion investor swimsuit for $44 million.

The place they’re now: With its COVID booster nonetheless in late-stage improvement and a number of other different DNA-based candidates together with HIV and most cancers medicines within the clinic, Inovio introduced in January that it deliberate to file an utility for its lead candidate, which treats recurrent respiratory papillomatosis, below the FDA’s accelerated approval program. However the firm hit a snag when the appliance was delayed because of manufacturing issues associated to its supply gadget.

Inovio is now concentrating on mid-2025 to submit its utility, in line with an earnings report launched this week. The corporate additionally famous that its money runway at present extends into the third quarter of subsequent yr.

Veru

The backstory: Even with a number of authorised vaccines available on the market, hospitalization and loss of life charges from COVID remained stubbornly excessive in 2022 — a problem Veru appeared poised to deal with with its antiviral and anti inflammatory remedy sabizabulin. The truth is, Veru halted its research of the drug in April 2022 as a result of the outcomes have been so optimistic it was deemed unethical to proceed administering a placebo to sufferers.

With handsome security and efficacy information in hand, Veru strode confidently into Emergency Use Authorization talks with the FDA and ready to commercialize the drug for acute respiratory misery syndrome.

But it surely wasn’t meant to be. In November 2022, an FDA adcomm voted towards approval because of the small pattern measurement of Veru’s sabizabulin trial, and Veru reported in March 2023 that the company had denied its EUA utility.

The place they’re now: Whereas the FDA supplied Veru steering on designing a confirmatory part 3 trial for sabizabulin, it has since stopped improvement till it receives funding from “authorities grants, pharmaceutical firm partnerships or different related third-party exterior sources,” the corporate mentioned in an e-mail.

As an alternative, Veru, which has one commercialized product within the sexual well being market, has jumped into the red-hot GLP-1 enviornment. With late-stage improvement for sabizabulin in breast most cancers additionally paused, Veru is throwing its medical power behind a selective androgen receptor modulator known as enobosarm.

“Our objective with enobosarm is to protect muscle mass whereas sufferers are on remedy with GLP-1s,” the corporate mentioned. “We’re at present in a part 2b research with information anticipated in January 2025.”