There was some debate over the latest resolution by the U.S. Division of the Treasury to ask the Fed to return unused CARES Act funding by December 31. Whatever the politics concerned, the choice shouldn’t essentially be a priority for buyers with a set earnings portfolio. However that doesn’t imply there aren’t any implications to be thought-about concerning portfolio investments.

The precise applications ending are the Major Market Company Credit score Facility, the Secondary Market Company Credit score Facility, the Municipal Liquidity Facility, the Predominant Road Lending Program, and the Time period Asset-Backed Securities Mortgage Facility. There’s no want to recollect these names, however it’s vital to know what these applications did for the markets, notably the mounted earnings market.

An Efficient Backstop

In March, the CARES Act created these applications to supply a backstop for the markets. They had been supposed to supply corporations, municipalities, and a few small companies with the money wanted to outlive the lockdowns, in case their regular sources of financing dried up on account of buyers pulling out of the market. Following the announcement of the applications, many didn’t go into impact for a couple of months. Nonetheless, their supposed impact occurred instantly. The markets stabilized and firms had been capable of get market financing at affordable rates of interest. As proven within the chart under, yields on investment-grade company bonds fell from a excessive of 4.6 % on March 20 to 2.7 % on April 20. They continued to fall and, as of December 16, had dropped to 1.81 %, simply above the all-time low of 1.80% in November.

Funding-Grade Company Bond Yields

Supply: Bloomberg Barclays U.S. Combination Bond Index, Company Yield to Worst

Simply realizing these applications had been accessible triggered the market to step in. Nearly all of allotted funds was not put into motion. In whole {dollars}, the cash loaned by the mixed applications was slightly below $25 billion, in line with the Fed’s most up-to-date assertion, made on November 30. But $1.95 trillion in program funding was initially allotted to those applications.

A Completely different Surroundings

Although COVID-19 case counts are rising considerably within the U.S., prompting new shutdowns in sure states, the financial surroundings is totally different at present than it was in March. At first of the pandemic, uncertainty as to the size or breadth of the financial disaster was a lot increased. The backstop applications gave buyers confidence that corporations would be capable of get financing in the event that they wanted it. Many companies had been capable of survive, notably those who had been wholesome previous to the disaster. Now, though uncertainty nonetheless exists as to the toll of the virus, we have now a very good sense of the measures that governments will take to sluggish the pandemic and which industries will likely be most affected. Given the approval of efficient vaccines, we even have a greater sense of the potential size of the disaster. So, we are able to see that key variations now exist that have an effect on the necessity for these CARES Act applications.

Company Survivability

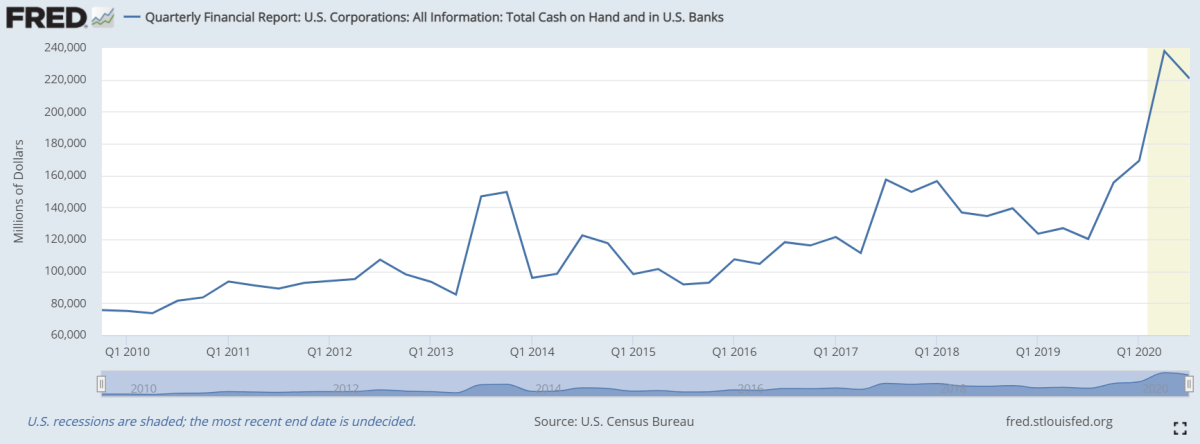

What does this imply for the markets? Buyers have extra confidence that investment-grade corporations will be capable of survive. Although some small companies and high-yield corporations might wrestle to rebound, the timeframe for the disaster just isn’t an entire unknown. Additionally, throughout this time-frame, many corporations had been capable of put together for a second wave of the virus. They accessed capital markets and refinanced or, with rates of interest traditionally low, took on further debt. In response to Barclays, from March by way of November of this 12 months, investment-grade corporations borrowed $1.4 trillion in debt, in comparison with solely $788 billion throughout the identical interval in 2019. To have the ability to survive a sluggish interval, corporations stored a considerable amount of the funds borrowed in money. The chart under from the St. Louis Fed exhibits the overall money readily available and in banks for U.S. firms.

What Are the Implications Shifting Ahead?

Though the CARES Act backstop applications are closing, the Fed stays dedicated to utilizing its conventional instruments to help the markets. They embrace retaining short-term rates of interest at 0 % for a number of years and persevering with to buy Treasuries and company mortgage-backed securities till we’re a lot nearer to full employment. These instruments will assist preserve rates of interest down. That may assist customers be capable of refinance their debt and have the arrogance to proceed spending. Whereas the backstop applications will likely be gone, Congress may restart them if we get a big shock to the markets. In any case, we noticed how efficient they had been in supporting companies through the first disaster. Going ahead, companies will likely be judged on their means to repay their loans over the long run. On condition that investment-grade corporations have largely refinanced any debt coming due, they need to proceed to exhibit low default charges within the close to time period.

With mounted earnings yields falling so low, many buyers could also be trying to discover investments that pay an inexpensive earnings. When contemplating this technique, it’s clever to maintain a couple of issues in thoughts. When transferring away from short-term investments to get increased yields, you need to contemplate the basics of particular person companies. Lively administration of mounted earnings can play a task right here, provided that the Fed might not help the whole market, particularly lower-quality corporations. Because of this, when searching for stability within the mounted earnings portion of your portfolio, you might need to contemplate higher-quality companies for longer-term investments.

As Warren Buffett mentioned, “It’s solely when the tide goes out that you just be taught who’s been swimming bare.” For now, nonetheless, we’re nonetheless at excessive tide in mounted earnings.

Editor’s Word: The unique model of this text appeared on the Impartial Market Observer.