On Aug. 28, Wall Avenue held its breath because the world’s most necessary synthetic intelligence (AI) firm reported second-quarter earnings. I am speaking about Nvidia (NASDAQ: NVDA), in fact. Whereas every member of the “Magnificent Seven” is seen as an indicator for the course of all issues AI, Nvidia has emerged as maybe the business’s end-all-be-all barometer.

However worry not! As soon as once more, Nvidia silenced the doubters after posting one more spectacular earnings report. Nevertheless, whereas combing via the monetary and working metrics, I found one announcement that left me slightly perplexed.

Particularly, Nvidia’s board of administrators authorized a further $50 billion in share repurchases (this comes on high of a remaining $7.5 billion from a previous buyback program). There is a normal notion that inventory buybacks could be fairly favorable for traders. However within the case of Nvidia, I simply do not get it.

Beneath, I am going to break down some explanation why I feel Nvidia introduced the buyback and why I don’t see this transfer as a motive to purchase the inventory proper now.

Is Nvidia’s buyback a distraction?

One of many larger bulletins from Nvidia this 12 months was the corporate’s 10-for-1 inventory cut up, which occurred again in June. Since early September 2022, shares of Nvidia have risen over 750%. Because the inventory worth eclipsed $1,000 per share, constructing a place in Nvidia grew to become extra of a hurdle for some traders.

Generally, an organization will select to separate its inventory following these vital rises within the share worth. Though a inventory cut up doesn’t inherently change an organization’s market capitalization, the decrease split-adjusted worth is usually perceived as inexpensive and should encourage traders to purchase. In consequence, a inventory may truly develop into extra costly following a cut up as a bigger physique of traders begins to pour in.

This is not precisely the case with Nvidia inventory, although. Since shares started buying and selling on a split-adjusted foundation on June 10, Nvidia inventory has declined by about 2% (as of market shut on Sept. 2). I am going to concede {that a} 2% drop shouldn’t be a motive to panic. However with that stated, I’m slightly stunned that the cut up didn’t encourage a noticeable uptick in shopping for exercise and subsequently propel Nvidia’s valuation to new highs.

To be candid, I see the announcement of the buyback as considerably of a PR stunt and an effort to reinspire traders.

Does Nvidia’s buyback make strategic sense?

Think about watching a business during which a celeb you admire endorses a product, however later, you be taught that the movie star has by no means used the product and easily promoted it as a result of they had been paid a charge to take action. In a method, that is form of what is going on on with Nvidia proper now.

Whereas including to the prevailing buyback initiative would possibly give the impression that administration views the inventory as an excellent shopping for alternative and even undervalued, understand that insider promoting has develop into all the craze at Nvidia during the last couple of months. Executives, together with Nvidia’s CEO, Jensen Huang; govt vp of operations, Debora Shoquist; and board members Mark Stevens and Tench Coxe had been all promoting inventory when Nvidia shares had been using excessive earlier in the summertime.

Why must you purchase Nvidia inventory when these liable for producing shareholder worth are cashing out? Maybe this can be a harsh criticism, as Nvidia’s executives nonetheless personal massive chunks of inventory — making their internet price intently tied to the efficiency of the enterprise. Nonetheless, I’ve another considerations concerning the buyback.

Whereas Nvidia is finest identified for its graphics processing items (GPUs), not too way back, I wrote a bit on how the corporate is deploying its file income into progress initiatives exterior its core semiconductor and information heart companies. Furthermore, contemplating Nvidia’s closest competitor, Superior Micro Units (AMD), has made a number of notable acquisitions over simply the final couple of years, I might assume administration could be motivated to double down on analysis and growth, advertising, and different endeavors amid intensifying competitors. I might see these as extra prudent selections, contemplating Nvidia did should delay orders on its latest Blackwell GPUs resulting from a design flaw.

One final level I would wish to make pertains to competitors exterior of AMD. Nvidia can also be going through surging competitors from its personal clients — notably among the Magnificent Seven members. Electrical automobile (EV) producer Tesla depends closely on Nvidia chips to develop autonomous driving software program. However latest remarks from Elon Musk counsel Tesla is seeking to migrate away from Nvidia and maybe compete with the chip big sooner or later. Furthermore, each Amazon and Meta are growing investments in capital expenditures (capex), particularly in some initiatives revolving round designing their very own in-house semiconductor chips.

Is Nvidia inventory an excellent purchase proper now?

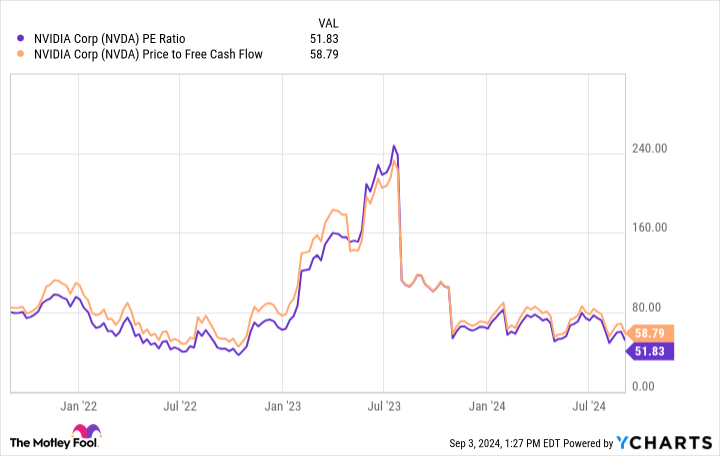

If you happen to take a look at Nvidia purely from a valuation perspective, there’s an argument to be made that the inventory is a cut price proper now. On price-to-earnings (P/E) and price-to-free money move (P/FCF) bases, Nvidia inventory is definitely inexpensive at this time than it was even only a few years in the past — and that is with all of this newfound income and revenue progress.

However I am starting to have some considerations that Nvidia is hard-pressed to determine alternatives to allocate capital amid a interval of rising competitors. I am not going to place forth the notion that investing in Nvidia is a disastrous alternative. I am going to save the doomsday-speak for an additional time.

Nevertheless, traders ought to understand that Nvidia’s file progress throughout the highest and backside traces is not going to final without end. Ultimately, progress will normalize and take a toll on Nvidia’s income. For that motive, I discover the $50 billion buyback questionable and never motive alone to scoop up shares of Nvidia in the meanwhile.

Do you have to make investments $1,000 in Nvidia proper now?

Before you purchase inventory in Nvidia, take into account this:

The Motley Idiot Inventory Advisor analyst group simply recognized what they imagine are the 10 finest shares for traders to purchase now… and Nvidia wasn’t one in every of them. The ten shares that made the lower may produce monster returns within the coming years.

Take into account when Nvidia made this checklist on April 15, 2005… when you invested $1,000 on the time of our suggestion, you’d have $630,099!*

Inventory Advisor supplies traders with an easy-to-follow blueprint for achievement, together with steering on constructing a portfolio, common updates from analysts, and two new inventory picks every month. The Inventory Advisor service has greater than quadrupled the return of S&P 500 since 2002*.

*Inventory Advisor returns as of September 3, 2024

Randi Zuckerberg, a former director of market growth and spokeswoman for Fb and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Idiot’s board of administrators. John Mackey, former CEO of Entire Meals Market, an Amazon subsidiary, is a member of The Motley Idiot’s board of administrators. Adam Spatacco has positions in Amazon, Meta Platforms, Nvidia, and Tesla. The Motley Idiot has positions in and recommends Amazon, Meta Platforms, Nvidia, and Tesla. The Motley Idiot has a disclosure coverage.

Opinion: Nvidia’s $50 Billion Buyback Is Not a Cause to Purchase the Inventory Hand Over Fist. This is What I am Involved About. was initially revealed by The Motley Idiot