Rates of interest are seemingly transitioning to a brand new regular, which is totally different from the previous regular. In different phrases, all the projections that assume charges can be getting again to regular are mistaken—as a result of the definition of regular has modified.

Change is never a fast course of, although. Usually, it may be so gradual that you just don’t discover it till the change is kind of massive. The grass in my yard, for instance, doesn’t appear to develop till the weekend, when it instantly wants slicing. The identical concept has been true for rates of interest, which have been dropping for many years.

Wanting on the Lengthy Time period

Observe the long run development may be very clear. In the course of the previous 40 years or so, nonetheless, there have been ups and downs. Over a interval of 5 to 10 years, the development is far much less clear.

There are a few takeaways from the chart above. Most present buyers had their early life within the Nineties and 2000s, with some going again to the Nineteen Eighties. Throughout that point interval, charges have been sometimes within the 4 % to eight % vary, which is what most of us at a senior stage now consider as regular. You may see that concept of regular fairly clearly in analyst projections of the place charges are more likely to go, as virtually all of them put charges again into that vary over a while interval. The bias of “what I grew up with” is a powerful one. However as you may see, that concept of regular was not very regular in any respect. My youthful colleagues, for instance, have seen charges of two % to three % as regular for all of their careers. Is that the brand new regular?

What Does Current Knowledge Say?

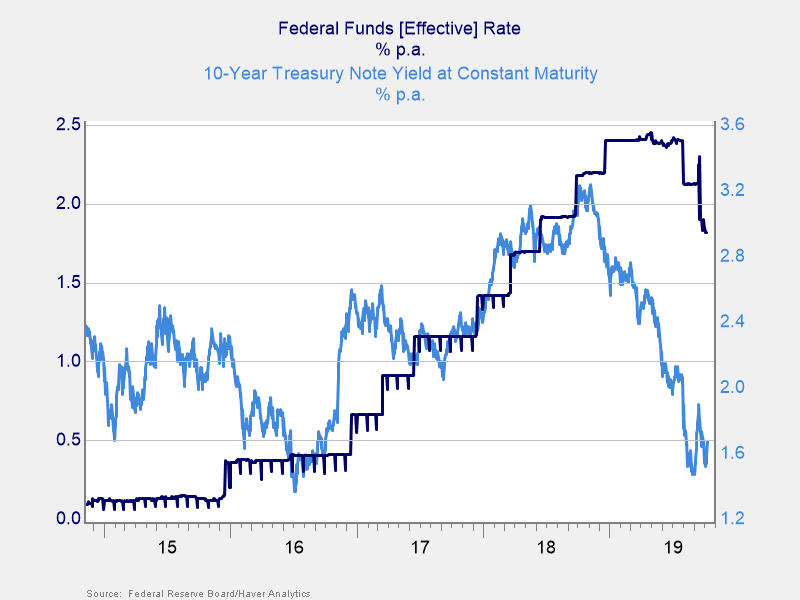

That vary could be the brand new regular, primarily based on the latest information. That 40-year chart is compelling, however current information seems to be a bit totally different. In 2016, the Fed began elevating charges, and the 10-year price adopted go well with. From 2016 via 2018, it seemed like we have been headed again to the traditional 4 % to six % that folks of my age (who, not coincidentally, run the Fed) anticipated. However then, in late 2018, one thing occurred. Whereas the Fed stored its charges up, the 10-year collapsed once more. Regular as soon as once more seemed not so regular. Fairly than the Fed setting rates of interest, it’s now responding to the market by slicing. No matter the brand new regular is, it’s extra highly effective than the Fed—so we’ve to take it critically.

What does this shift imply for the longer term? Is there a brand new regular? How can we inform? And what’s going to or not it’s? Clearly, the expectations that charges would rise again to regular is, at the very least, unsure.

Not Only a U.S. Story

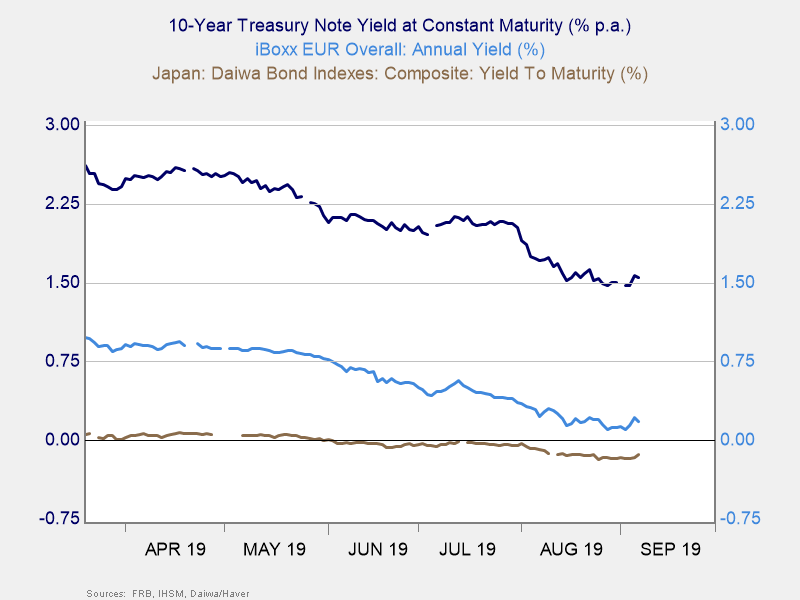

Around the globe, we see charges each very low by historic ranges (after many years of declines) and down considerably prior to now 6 to 12 months. No matter is happening is occurring all over the world, and any clarification must account for that. Past that, our clarification must account for why charges are so totally different between space markets. Because the chart beneath reveals, U.S. charges are properly above European charges, that are properly above Japanese charges, that are beneath zero collectively. We want some form of clarification as to why that must be. In financial concept, in a world capital market, charges ought to converge, which isn’t occurring. In financial observe, regular charges are assumed, and that isn’t occurring both.

The place We Are (and The place We Would possibly Be Going)

Charges have been dropping for many years. Regular, as many people give it some thought, isn’t occurring—and isn’t more likely to occur. On prime of that, totally different areas have very totally different rates of interest; primarily based on financial concept, this shouldn’t occur. Economics doesn’t give us good steering as to what’s occurring—or what’s more likely to occur.

So, possibly one thing else is happening. Tomorrow, we’ll check out the totally different ways in which rates of interest could also be set to start out to determine what that “one thing else” could be.

Editor’s Observe: The unique model of this text appeared on the Unbiased Market Observer.