One of many investing methods rising in reputation with the rich is Direct Indexing. Earlier than my consulting stint at a fintech startup in 2024, I had by no means actually heard of Direct Indexing. If I did, I seemingly assumed it merely meant straight investing in index funds, which many people already do.

Nonetheless, Direct Indexing is extra than simply shopping for index funds. It’s an funding technique that permits traders to buy particular person shares that make up an index reasonably than shopping for a standard index fund or exchange-traded fund (ETF). This strategy allows traders to straight personal a personalized portfolio of the particular securities throughout the index, offering larger management over the portfolio’s composition and tax administration.

Let us take a look at the advantages and disadvantages of Direct Indexing to get a greater understanding of what it’s. In a manner, Direct Indexing is solely a brand new technique to bundle and market funding administration companies to purchasers.

Advantages of Direct Indexing

- Personalization: Direct Indexing permits you to align your portfolio together with your particular values and monetary targets. For instance, you’ll be able to exclude all “sin shares” out of your portfolio if you want.

- Tax Optimization: This technique provides alternatives for tax-loss harvesting that might not be out there with conventional index funds. Tax-loss harvesting helps reduce capital beneficial properties tax legal responsibility, thereby boosting potential returns.

- Management: Buyers have extra management over their investments, permitting them to handle their publicity to specific sectors or corporations. As an alternative of following the S&P 500 index managers’ selections on firm choice and weighting, you’ll be able to set sector weighting limits, for instance.

Drawbacks of Direct Indexing

- Complexity: Managing a portfolio of particular person shares is extra advanced than investing in a single fund. Due to this fact, most traders don’t do it themselves however pay an funding supervisor to deal with it, which results in extra charges.

- Value: The administration charges and buying and selling prices related to Direct Indexing may be increased than these of conventional index funds or ETFs, though these prices could also be offset by tax advantages.

- Minimal Funding: Direct Indexing typically requires a better minimal funding, making it much less accessible for some traders.

- Efficiency Uncertainty: It is exhausting to outperform inventory indices just like the S&P 500 over the long run. The extra an investor customizes with Direct Indexing, doubtlessly, the larger the underperformance over time.

Who Ought to Contemplate Direct Indexing?

Direct indexing is especially fitted to high-net-worth people, these in increased tax brackets, or traders in search of extra management over their portfolios and keen to pay for the customization and tax advantages it provides.

For instance, if you’re within the 37% marginal revenue tax bracket, face a 20% long-term capital beneficial properties tax, and have a internet value of $20 million, you might need robust preferences in your investments. Suppose your mother and father had been hooked on tobacco and each died of lung most cancers earlier than age 60; consequently, you’d by no means need to personal tobacco shares.

An funding supervisor might customise your portfolio to intently observe the S&P 500 index whereas excluding all tobacco and tobacco-related shares. They might additionally usually conduct tax-loss harvesting to assist reduce your capital beneficial properties tax legal responsibility.

Nonetheless, if you’re in a tax bracket the place you pay a 0% capital beneficial properties tax fee and haven’t got particular preferences in your investments, direct indexing might not justify the extra price.

This state of affairs is much like how the mortgage curiosity deduction was extra advantageous for these in increased tax brackets earlier than the SALT cap was enacted in 2018. Whether or not the SALT cap shall be repealed or its $10,000 deduction restrict elevated stays to be seen, particularly given its disproportionate influence on residents of high-cost, high-tax states.

Extra Individuals Will Achieve Entry to Direct Indexing Over Time

Fortunately, you don’t have to be value $20 million to entry the Direct Indexing technique. When you’re a part of the mass prosperous class with $250,000 to $2 million in investable belongings, you have already got sufficient. As extra fintech corporations broaden their product choices, much more traders will have the ability to entry Direct Indexing.

Simply as buying and selling commissions finally dropped to zero, it’s solely a matter of time earlier than Direct Indexing turns into extensively out there to anybody . Now, if solely actual property commissions might hurry up and in addition turn into extra cheap.

Which Funding Managers Supply Direct Indexing

So that you consider in the advantages of Direct Indexing and need in. Beneath are the varied corporations that supply Direct Indexing companies, the minimal you have to get began, and the beginning charge.

As you’ll be able to see, the minimal funding quantity to get began ranges from as little as $100,000 at Charles Schwab and Constancy to $250,000 at J.P. Morgan, Morgan Stanley, and different conventional wealth manages.

In the meantime, the beginning charge ranges between 0.20% to 0.4%, which can get negated by the extra funding return projected by direct indexing tax administration. The charge is normally on prime of the associated fee to carry an index fund or ETF (minimal) or inventory (zero).

Now that we’re conscious of the number of corporations providing Direct Indexing, let’s delve deeper into the tax administration side. The advantages of personalization and management are simple: you set your funding parameters, and your funding managers will attempt to speculate in accordance with these tips.

Understanding Tax-Loss Harvesting

Tax-loss harvesting is a method designed to cut back your taxes by offsetting capital beneficial properties with capital losses. The larger your revenue and the wealthier you get, usually, the larger your tax legal responsibility. Rationally, all of us need to hold extra of our hard-earned cash than giving it away to the federal government. And the extra we disagree with the federal government’s insurance policies, the extra we are going to need to reduce taxes.

Primary tax-loss harvesting is comparatively easy and may be carried out independently. As your revenue will increase, triggering capital beneficial properties taxes—extra superior methods turn into out there, typically requiring a portfolio administration charge.

Primary Tax-Loss Harvesting

Annually, the federal government permits you to “understand” as much as $3,000 in losses to cut back your taxable revenue. This discount straight decreases the quantity of taxes you owe.

For instance, in case you invested $10,000 in a inventory that depreciated to $7,000, you could possibly promote your shares at $7,000 earlier than December thirty first to cut back your taxable revenue by $3,000. You’ll be able to carry over $3,000 in annual losses till it’s exhausted.

Anyone who does their very own taxes or has somebody do their taxes for you’ll be able to simply conduct fundamental tax-loss harvesting.

Superior Tax-Loss Harvesting

Superior tax-loss harvesting, nonetheless, is barely extra sophisticated. It might’t be used to cut back your revenue straight, however it may be utilized to cut back capital beneficial properties taxes.

As an illustration, in case you purchased a inventory for $100,000 and offered it for $150,000, you’d have a realized capital achieve of $50,000. This achieve can be topic to taxes primarily based in your holding interval:

- Brief-term capital beneficial properties: If the inventory was held for lower than a 12 months, the achieve can be taxed at your marginal federal revenue tax fee, which is identical fee as your common revenue.

- Lengthy-term capital beneficial properties: If the holding interval exceeds one 12 months, the achieve can be taxed at a decrease long-term capital beneficial properties fee, which is usually extra favorable than your marginal fee.

To mitigate capital beneficial properties taxes, you’ll be able to make the most of tax-loss harvesting by promoting a inventory that has declined in worth to offset the beneficial properties from a inventory that has appreciated. There isn’t any restrict on how a lot in beneficial properties you’ll be able to offset with realized losses. Nonetheless, when you promote a inventory, you have to wait 30 days earlier than repurchasing it to keep away from the “wash sale” rule.

When To Use Tax-Loss Harvesting

Within the instance above, to offset $50,000 in capital beneficial properties, you would wish to promote securities at a loss throughout the identical calendar 12 months. The deadline for realizing these losses is December thirty first, guaranteeing they’ll offset capital beneficial properties for that particular 12 months.

As an illustration, in case you had $50,000 in capital beneficial properties in 2023, promoting shares in 2024 with $50,000 in losses would not eradicate your 2023 beneficial properties. The capital beneficial properties tax would nonetheless apply when submitting your 2023 taxes. To offset the beneficial properties in 2023, you’d have wanted to promote shares in 2023 with $50,000 in losses.

Nonetheless, for example you had $50,000 in capital beneficial properties after promoting inventory in 2024. Even in case you did not incur any capital losses in 2024, you could possibly use capital losses from earlier years to offset these beneficial properties.

Sustaining correct data of those losses is essential, particularly in case you’re managing your individual investments. When you rent an funding supervisor, they may monitor and apply these losses for you.

Essential Level: Capital Losses Can Be Carried Ahead Indefinitely

In different phrases, capital losses may be carried ahead indefinitely to offset future capital beneficial properties, supplied they have not already been used to offset beneficial properties or cut back taxable revenue in prior years.

Throughout a number of years in my 20s, I used to be unaware of this. I mistakenly believed that I might solely carry over a $3,000 loss to deduct in opposition to my revenue every year. In consequence, I paid hundreds of {dollars} in capital beneficial properties taxes that I did not must pay. If I had a wealth supervisor to help me with my investments, I’d have saved a big amount of cash.

Whereas the best holding interval for shares could also be indefinite, promoting sometimes might help fund your required bills. Tax-loss harvesting goals to attenuate capital beneficial properties taxes, enhancing your general return and offering extra post-tax shopping for energy.

The upper your revenue tax bracket, the extra helpful tax-loss harvesting turns into.

Tax Bracket Influence And Direct Indexing

Your marginal federal revenue tax bracket straight influences your tax legal responsibility. Shielding your capital beneficial properties from taxes turns into extra advantageous as you progress into increased tax brackets.

As an illustration, in case your family revenue is $800,000 (prime 1% revenue), inserting you within the 37% federal marginal revenue tax bracket, a $50,000 short-term capital achieve from promoting Google inventory would lead to an $18,500 tax legal responsibility. Conversely, a $50,000 long-term capital achieve can be taxed at 20%, amounting to a $10,000 tax legal responsibility.

Now, for example your married family earns a middle-class revenue of $80,000, inserting you within the 12% federal marginal revenue tax bracket. A $50,000 short-term capital achieve from promoting Google inventory would incur an $11,000 tax legal responsibility—$7,500 lower than in case you had been making $800,000 a 12 months. In the meantime, a $50,000 long-term capital achieve can be taxed at 15%, or $7,500.

On the whole, attempt to maintain securities for longer than a 12 months to qualify for the decrease long-term capital beneficial properties tax fee. Because the examples illustrate, the upper your revenue, the larger your tax legal responsibility, making direct indexing and its tax administration methods extra helpful.

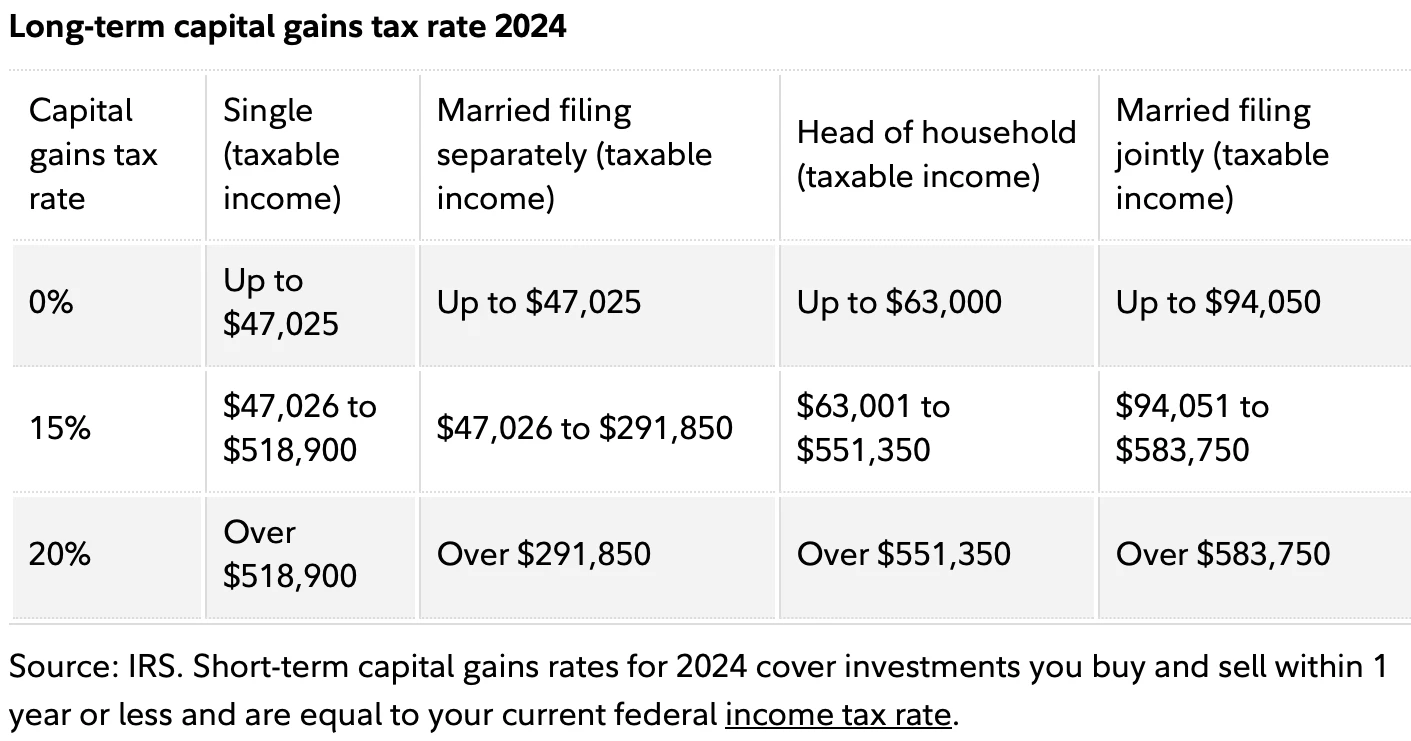

Beneath are the revenue thresholds by family kind for long-term capital beneficial properties tax charges in 2024.

Restrictions and Guidelines for Tax-Loss Harvesting

Hopefully, my examples clarify the advantages of tax-loss harvesting. For large capital beneficial properties and losses, tax-loss harvesting makes a whole lot of sense to enhance returns. I am going to at all times bear in mind shedding huge bucks on my investments, and utilizing these losses to salvage any future capital beneficial properties.

Nonetheless, tax-loss harvesting can get sophisticated in a short time in case you interact in lots of transactions through the years. By December thirty first, you have to resolve which underperforming shares to promote to offset capital beneficial properties and reduce taxes. That is the place having a wealth advisor managing your investments turns into extra helpful.

For do-it-yourself traders, the problem lies within the time, expertise, and data wanted for efficient investing. When you plan to have interaction in tax-loss harvesting, let’s recap the necessities to make issues crystal clear.

Annual Tax Deduction Carryover Restrict is $3,000

- When you have $50,000 in capital losses and $30,000 in whole capital beneficial properties for the 12 months, you should use $30,000 in capital losses to offset the corresponding beneficial properties, leaving you with $20,000 in remaining capital loss.

- You’ll be able to carry over the remaining $20,000 in losses indefinitely to offset future beneficial properties. In years with out capital beneficial properties, you should use your capital loss carryover to deduct as much as $3,000 a 12 months in opposition to your revenue till it’s exhausted.

No Expiration Date on Capital Losses

- When you have $90,000 in capital losses from promoting shares throughout a bear market and 0 capital beneficial properties that 12 months, you’ll be able to carry these losses ahead to offset future revenue or capital beneficial properties. Luckily, capital losses by no means expire.

The Wash Sale Rule Nullifies Tax-Loss Harvesting Advantages

- A loss is disallowed if, inside 30 days of promoting the funding, you or your partner reinvest in an similar or “considerably related” inventory or fund.

Losses Should First Offset Features of the Similar Kind

- Brief-term capital losses should first offset short-term capital beneficial properties, and long-term capital losses should offset long-term beneficial properties. If losses exceed beneficial properties, the remaining capital-loss steadiness can offset private revenue as much as a restricted quantity. For detailed recommendation, seek the advice of a tax skilled.

Direct Indexing Conclusion

Personalization, management, and tax optimization are the important thing advantages of Direct Indexing. With this strategy, you do not have to spend money on sectors or corporations that do not align together with your beliefs. Nor do you must blindly observe the sector weightings of an index fund or ETF as they modify over time. This represents the personalization and management features of Direct Indexing.

When you’re centered on return optimization, the tax-loss harvesting function of Direct Indexing is most engaging. In accordance with researchers at MIT and Chapman College, tax-loss harvesting yielded an extra 1% annual return on common from 1928 to 2018. Even when Direct Indexing prices as much as 0.4% yearly, the advantages of tax-loss harvesting nonetheless outweigh the associated fee.

One of the simplest ways to keep away from paying capital beneficial properties taxes is to chorus from promoting. Borrow out of your belongings like billionaires to pay much less taxes. Nonetheless, when you have to promote shares to boost your life, bear in mind the benefits of tax-loss promoting, as it may well considerably cut back your tax liabilities.

Direct Indexing provides a compelling technique to optimize returns by tax-loss harvesting and portfolio customization. As tax legal guidelines turn into extra advanced and traders search methods to align their portfolios with private values, Direct Indexing gives a strong software for each superior and on a regular basis traders.

Reader Questions

Have you ever used the technique of Direct Indexing earlier than? Was this the primary time you’ve heard of it? Do you assume the advantages of tax-loss harvesting justify the extra charges related to Direct Indexing? I consider that finally, Direct Indexing will turn into out there to a broader viewers at a decrease price.

With inventory market volatility returning and a possible recession looming, it is extra necessary than ever to get a monetary checkup. Empower is presently providing a free monetary session with no obligation for a restricted time.

When you have over $250,000 in investable belongings, do not miss this chance. Schedule an appointment with an Empower skilled right here. Full your two video calls with the advisor earlier than October 31, 2024, and you may obtain a free $100 Visa present card. There isn’t any obligation to make use of their companies after.

Empower provides a proprietary indexing methodology referred to as Good Weighting to its purchasers. Good Weighting samples particular person U.S. shares to create an index that equally weights financial sector, model, and dimension. The purpose is to attain a greater risk-adjusted return.

The assertion is supplied to you by Monetary Samurai (“Promoter”) who has entered right into a written referral settlement with Empower Advisory Group, LLC (“EAG”). Click on right here to be taught extra.