In our final weblog, “The perfect defence is an effective offence”, we mentioned the drivers behind the expansion in European financial institution consolidation exercise. Right here, we discover how consolidation can profit financial institution bond traders, and establish the place additional consolidation is probably to happen. We begin by contemplating European home markets earlier than evaluating the potential for cross-border consolidation, which plenty of European policymakers have publicly inspired. Lastly, we look at the US, assessing how final 12 months’s regional financial institution disaster and doable regulatory modifications might have an effect on mergers and acquisitions (M&A) in that market.

Why consolidation can profit credit score traders

Following the International Monetary Disaster, we noticed consolidation ensuing from weaker banks being rescued. M&A is now extra strategic, with completely different drivers, as famous in our earlier weblog publish. We might argue {that a} wholesome, however not extreme, degree of consolidation creates a stronger banking system, benefitting financial institution credit score traders. Banks in additional consolidated markets are inclined to have extra scale, enabling extra funding and lowering the probability of dangerous pricing wars seen in additional fragmented markets. The banks will even be extra systemically vital, going through elevated regulatory oversight and focus.

Taking Eire for example…

Consolidation within the Irish banking market culminated with the exit of KBC and NatWest in 2022, leaving the highest three banks (Allied Irish Financial institution, Financial institution of Eire, and Everlasting TSB) with a mixed mortgage market share exceeding 80%. Everlasting TSB, which noticed its mortgage mortgage ebook improve by 40% with the Ulster (NatWest) loans acquisition, achieved an funding grade senior unsecured ranking with Moody’s shortly after the mixture, with Fitch following in 2024. It at present has its rankings on constructive outlook with each Moody’s and S&P.

Though many components contributed to the Irish banks’ rags-to-riches tales, together with vital deleveraging within the financial system, consolidation has performed an element. It’s also possible a cause why the Irish banks have handed on much less of the central financial institution’s base price will increase to depositors than UK banks, which function in a extra fragmented market, thereby enhancing their profitability. Nevertheless, the aggressive panorama stays fluid, with new entrants like Spanish financial institution Bankinter, which already offers mortgage and shopper loans within the native Irish retail market, making use of for a banking licence to supply native deposits.

The place in Europe might we see extra home consolidation?

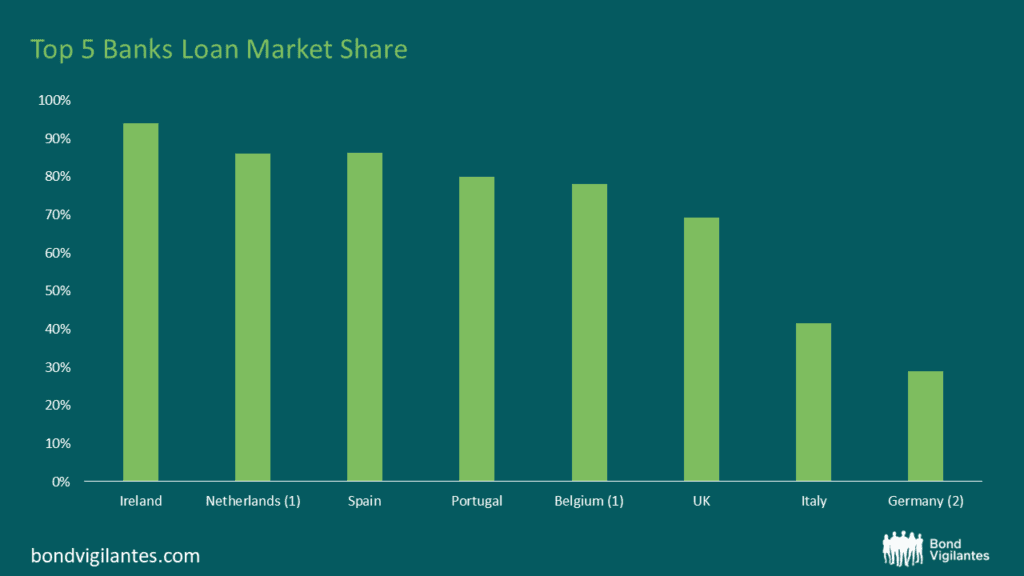

The chart under exhibits the various levels of banking sector focus in Western Europe, with Italy and Germany among the many least concentrated. We talk about the probability of consolidation in each of these nations in addition to the prospects in different elements of Europe.

Italy

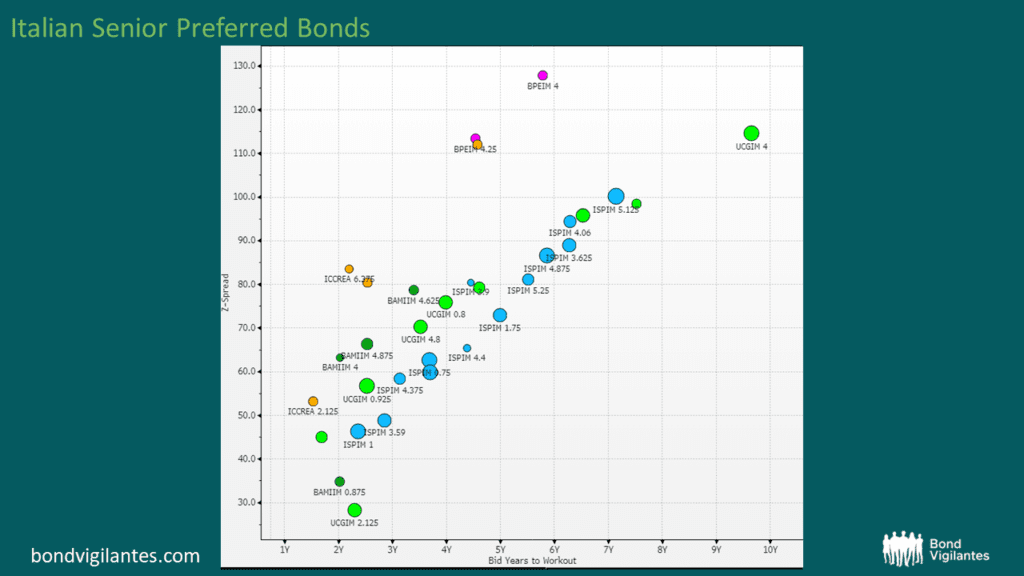

Italy is one area the place we might see additional consolidation. As seen within the chart above, banking focus is comparatively low in Italy. The Italian authorities has began a gradual sell-down of Banca Monte dei Paschi di Siena and is eager to discover a purchaser, as this is able to speed up the exit. A few of the small to mid-sized Italian banks may be targets. The chart under exhibits Banco BPM most popular senior spreads buying and selling near these of the Nationwide champions (Intesa Sanpaolo and Unicredit), suggesting the bond market views it as a possible takeover goal.

Germany

Germany is among the many least consolidated banking methods in Europe. Nevertheless, additional consolidation is difficult by Germany’s “3 Pillar” banking system, the place two of the “Pillars” (the financial savings banks and cooperative sector) are non-profit maximising organisations, making up roughly 60% of the market. Consolidation throughout the three pillars is troublesome as a result of differing possession constructions and political, authorized and regulatory components. Privately-owned and listed German banks (like Deutsche Financial institution and Commerzbank) solely make up roughly 30% of the market and consolidation inside this phase is feasible. Deutsche Financial institution has beforehand checked out buying Commerzbank and one other try sooner or later can’t be dominated out. Unicredit has additionally been rumoured to be fascinated by Commerzbank, the place it might merge it with its German subsidiary, HVB. Not like in Italy, we don’t suppose the credit score spreads of German banks are at present pricing in any consolidation.

Different EU nations

The banking methods of Portugal and the Netherlands, that are already fairly concentrated, might turn out to be a little bit extra so, as they’ve banks on the market. Novo Banco in Portugal and De Volksbank within the Netherlands could possibly be purchased, although their respective house owners might select an preliminary public providing (IPO) exit fairly than M&A.

In Spain, which has already undergone a number of waves of consolidation, the federal government has expressed some discomfort with the mixture of BBVA and Sabadell though they’ve but to formally block that merger. That mentioned, additional consolidation of smaller subscale gamers in Spain shouldn’t be dominated out.

European Cross-Border M&A: is it a pipe dream?

The European Central Financial institution (ECB) has usually cited the advantages of cross-border M&A inside the EU. In a speech final 12 months, the previous Head of ECB-SSM, Andrea Enria, highlighted three advantages:

- Non-public threat sharing – the place cross-border banks are capable of higher take up losses in comparison with native banks.

- Smoother decision of failing banks in an built-in European market, as a failing financial institution’s belongings/liabilities might extra simply be transferred to a bigger set of potential bidders.

- Decrease correlation of dangers between the house sovereign and the financial institution.

Whereas these advantages will be vital, we don’t anticipate to see a lot cross-border M&A within the EU anytime quickly. Enria himself acknowledges among the challenges, together with the difficulties in extracting synergies when banks should preserve international operations out of subsidiaries fairly than branches. With subsidiaries, native regulators often have their very own liquidity and capital necessities, which might restrict the advantages of scale to the mother or father organisation. Different components embrace authorized variations (e.g. shopper rights, insolvency guidelines), negligible alternative to consolidate branches (little overlap), and cultural/language variations.

European regulators try to harmonise some guidelines, akin to these round “depositor choice” (the place of depositors within the creditor hierarchy in decision). Nevertheless, we expect cross-border M&A is extra prone to stay confined to banking teams buying operations in nations by which they have already got a presence, akin to bolt-on, asset-light, fee-income-generating acquisitions, or partnerships akin to in wealth administration or absolutely digital initiatives with a small scale. Examples of the previous embrace Credit score Agricole’s enlargement in Italy or extra just lately the Belgian financial institution, KBC, which merged its Bulgarian financial institution UBB with RBI (Bulgaria) in 2022, rising its native market share from 14% to 19%.

US: Regulation change might encourage extra consolidation, however the end result of the Capital One and Uncover regulatory approval course of will probably be vital

The US has over 4,000 banks so we are going to very possible see extra consolidation, particularly among the many smaller establishments. The scenario with bigger banks is completely different, nevertheless. There are numerous regulatory hurdles for the so-called “G-SIBS” (International Systemically Vital Establishments), however there was, and can absolutely be, extra consolidation amongst bigger regionals. Elevated regulatory scrutiny on regional banks with belongings over $100 billion might encourage consolidation, as it could be extra environment friendly for these near the $100 billion asset threshold to leap over it fairly than crawl over it. Nevertheless, uncertainty round regulatory and political urge for food for financial institution mergers is at present posing considerably of a roadblock. Capital One has launched a takeover bid for Uncover which might, if accepted, open the door for different M&A on this phase. Whereas we imagine the argument for extra consolidation is robust (scale, synergies, and so on.), regulators’ views may have a major impression on US financial institution M&A exercise. For instance, Toronto Dominion known as off its $13.4bn takeover of First Horizon in 2023 attributable to uncertainty about regulatory approvals. Ought to such approvals for giant regional M&A show troublesome, banks might choose to develop organically or by buying a lot smaller establishments as an alternative.

To sum up, we imagine a wholesome degree of consolidation is constructive for financial institution bond traders. Nevertheless, in Europe, regardless of some key policymakers favouring EU cross-border consolidation, there are nonetheless too many hurdles to attaining this meaningfully. Subsequently, European financial institution consolidation will largely stay a “home affair” in the intervening time. Whereas within the US, the result of the Capital One acquisition of Uncover will probably be key in figuring out how a lot M&A we are going to see within the close to time period.