Lately, the transmission mechanism of financial coverage—the intricate course of via which central financial institution actions affect the economic system—has undergone important adjustments, notably as international debt ranges have surged. With governments all over the world carrying heavier debt burdens, the affect of rising rates of interest on the economic system has shifted in ways in which policymakers should grapple with. This complicated scenario underscores the necessity for a deeper understanding of the financial dynamics. One of the urgent points is the impact of accelerating curiosity funds on authorities debt, reshaping how central banks take into consideration and implement financial coverage.

The normal transmission mechanism

Traditionally, central banks have used rates of interest as their main instrument to affect financial exercise. When inflation is excessive, or the economic system is overheating, central banks elevate rates of interest to chill demand by making borrowing dearer. Conversely, when the economic system is sluggish, they decrease charges to stimulate spending and funding by making credit score cheaper.

This course of works via a number of channels:

- Rates of interest: increased charges improve the borrowing prices for companies and customers, lowering spending and funding, and vice versa.

- Wealth impact: adjustments in rates of interest have an effect on asset costs, which affect family wealth and, in flip, shopper spending.

- Alternate charges: increased rates of interest can entice overseas capital, strengthen the home forex, and affect commerce balances.

Nevertheless, with unprecedented ranges of presidency debt, the standard transmission of financial coverage is turning into more and more sophisticated.

The position of excessive debt in altering the transmission mechanism

Now authorities debt is at traditionally excessive ranges, the affect of rate of interest adjustments reverberates extra strongly via fiscal channels. Rising rates of interest have an effect on non-public debtors and considerably improve the price of servicing authorities debt. This creates a suggestions loop between financial and financial coverage, which can finally constrain the central financial institution’s skill to make use of its instruments as freely because it did previously.

Rising curiosity funds and the fiscal-monetary coverage nexus

As rates of interest rise, governments should allocate extra of their budgets to debt servicing prices. This presents a big dilemma: increased curiosity funds can crowd out different types of authorities spending, equivalent to infrastructure investments, social applications, or healthcare. In international locations with very excessive debt-to-GDP ratios, equivalent to the USA, Japan, and several other European nations, the price of debt servicing has turn out to be a considerable a part of the nationwide finances.

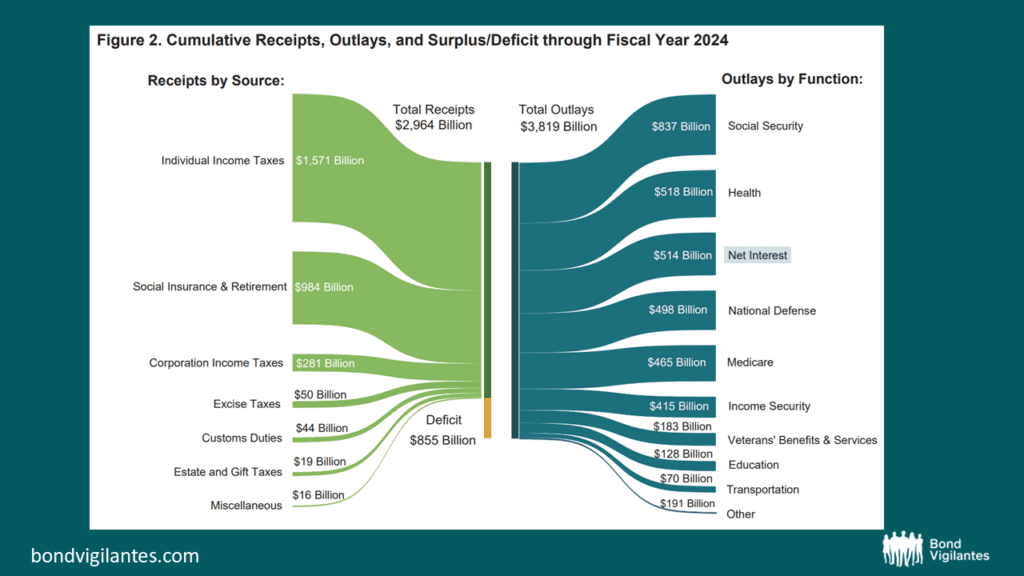

The determine under illustrates the substantial measurement of the US web curiosity expense. It’s on monitor to be the second largest outlay, second solely to Social Safety. Maybe for this reason Japan, with its 250% debt to GDP, has been so gradual to lift rates of interest.

This improve in authorities spending on curiosity funds as a result of rising charges means two issues:

- Constrained fiscal coverage: governments could have much less room to manoeuvre in relation to fiscal stimulus, as a bigger proportion of their income goes in the direction of curiosity funds. This might restrict the effectiveness of countercyclical fiscal measures in future recessions.

- Political strain on central banks: central banks could face political strain to maintain rates of interest low to assist cut back the federal government’s borrowing prices. This creates a danger of ‘fiscal dominance’, the place the necessity to handle authorities debt trumps the central financial institution’s give attention to controlling inflation.

The affect on financial development

The rising value of presidency debt may considerably dampen financial development. As governments are compelled to spend extra on debt servicing, they could reduce on productive investments that drive long-term financial development. The gravity of the scenario is a trigger for concern. Moreover, increased rates of interest can squeeze private-sector borrowing, particularly for small companies and customers, resulting in decrease ranges of financial exercise general.

How excessive debt impacts central financial institution choices

A central financial institution’s conventional goal is to handle inflation and stabilise the economic system. Nevertheless, with excessive debt ranges, central bankers should now additionally contemplate the fiscal implications of their actions. Elevating rates of interest aggressively to fight inflation might doubtlessly destabilise public funds, particularly if governments are already combating giant deficits and excessive debt hundreds.

For instance, a rustic with excessive debt that faces rising rates of interest may even see its credit standing downgraded, resulting in increased borrowing prices and a vicious cycle of debt accumulation. Central banks could also be compelled to undertake a extra cautious method to tightening financial coverage, even when inflation rises, to keep away from exacerbating fiscal pressures. This warning might result in a scenario of ‘fiscal dominance’, the place the central financial institution’s skill to regulate inflation is compromised by political strain to maintain rates of interest low for the federal government’s profit, highlighting the potential dangers to inflation management when central financial institution independence is threatened.

Altering coverage transmission

One other important shift within the transmission mechanism is that prime debt ranges have led to larger uncertainty about how rapidly or successfully financial coverage actions translate into financial outcomes and thru which channel—financial or fiscal.

Contemplate a situation the place a central financial institution hesitates to lift charges as a result of considerations over authorities debt. On this case, inflation might persist at excessive ranges, diminishing buying energy and undermining the efficacy of future coverage interventions. This erosion of the central financial institution’s management over inflation as a result of ‘fiscal dominance’ might lead to much less efficient future coverage interventions, highlighting the enduring affect of excessive debt ranges on the economic system.

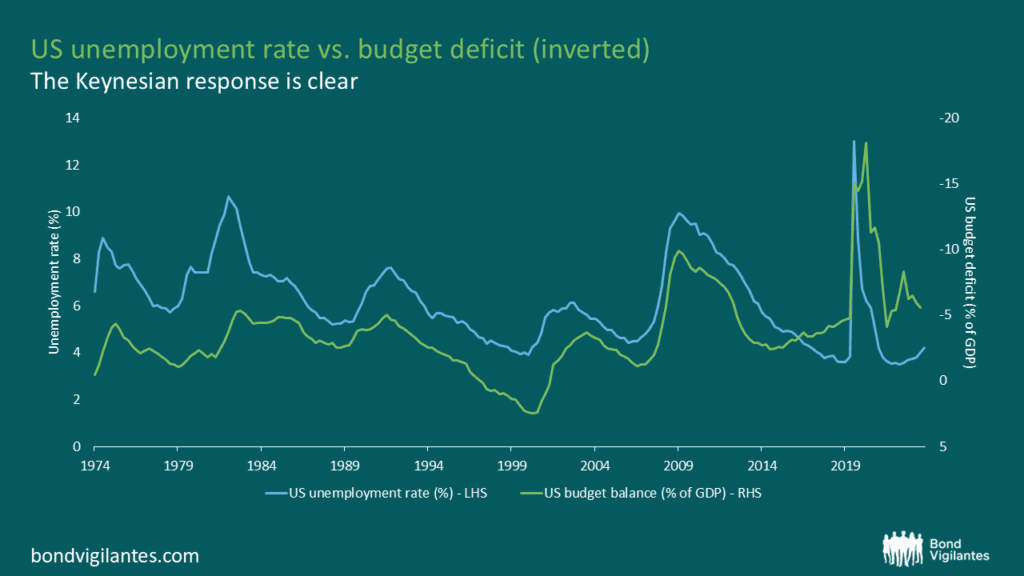

The US economic system, together with others, is approaching a important juncture, with the upcoming election doubtlessly serving as a catalyst. Regardless of being within the fourth yr of financial enlargement and with unemployment at or close to all-time lows, present deficit ranges mirror these seen throughout recessionary durations.

The chart under exhibits the unemployment price vs. the deficit (inverted):

When the following financial downturn arrives, the federal government could discover itself in a precarious scenario. Will it be capable of reply with a Keynesian splurge given the present ranges of debt and deficits? If the brand new administration fails to curb spending, the market could pressure austerity measures on the federal government. Fearing this final result, the federal government will seemingly must tighten fiscal spending, doubtlessly resulting in an financial slowdown.

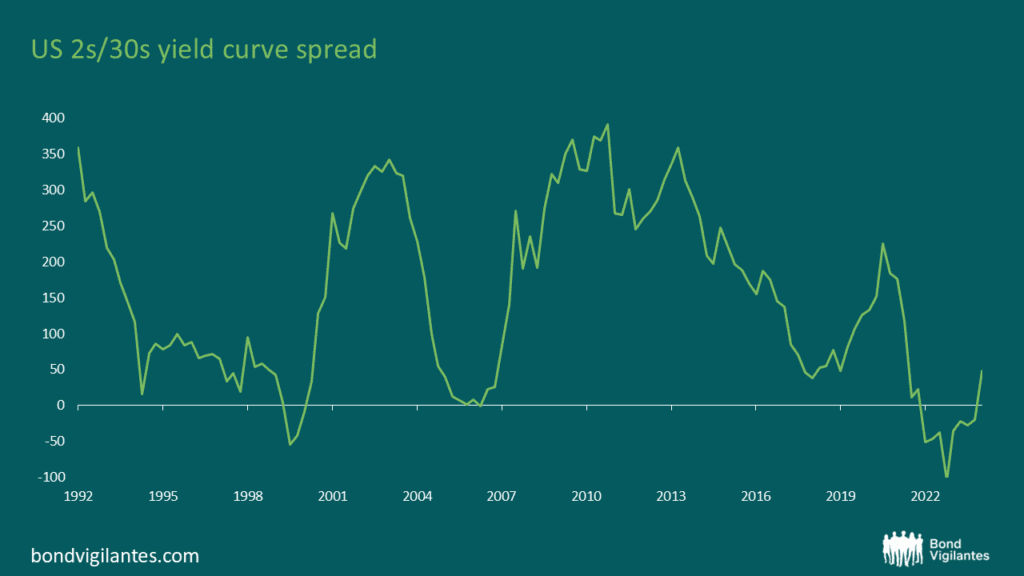

This dynamic has made life more and more tough for traders, and they need to stay cautious. With rates of interest beginning to transfer decrease on the again of price cuts and valuations trying stretched with nonetheless comparatively flat curves, mounted earnings is liable to yields transferring materially steeper as traders lose confidence or central banks reply to an financial slowdown.

From a long run perspective, the curve stays exceptionally flat:

Worryingly, politicians appear extra involved about individuals consuming canine and cats over the pending fiscal disaster. Maybe traders will proceed turning to different belongings equivalent to gold, which is understood to guard in opposition to inflation, forex devaluation and geopolitical danger, which appears to be rising by the day. Alternatively, we may even see a larger give attention to economies with sturdy fiscal positions and low excellent debt.