Over half of the world’s inhabitants have forged or will likely be casting their votes to elect their nation’s leaders in 2024. This contains elections in eight of the world’s most populous nations: India, the US, Indonesia, Pakistan, Brazil, Bangladesh, Russia, and Mexico. Wanting particularly at Indonesia, we’ll discover the historic political journey of the world’s largest archipelagic state from the period of Sukarno to the present ‘Reformasi’ interval, analyzing outgoing President Joko Widodo’s tenure and the current 2024 presidential election. We are going to have a look at the fiscal and financial challenges the brand new administration below incoming President Prabowo faces, the market’s response, and the essential function of infrastructure funding in Indonesia’s future. Whereas considerations about public debt and populist insurance policies persist, we’ll assess different market elements which will affect the course of the Indonesian bond market.

From Sukarno to Reformasi

Indonesia, the most important nation in Southeast Asia with a inhabitants of 280 million, had 204 million eligible voters forged their ballots on February 14 to elect its 8th President. This marks solely the fifth election since Indonesia grew to become an impartial republic in 1945. The primary president, Sukarno, held energy for 22 years after consolidating management and changing into ‘President for Life’. Nevertheless, years of financial hardship characterised by hyperinflation, and rising threats from communist ideologies, led to Sukarno being changed by one other authoritarian chief, President Suharto, who dominated from 1968 to 1998. Suharto was pressured to step down within the aftermath of the 1997 Asian Monetary Disaster as a result of extreme home financial instability, a collapsed forex, and unrest in numerous areas throughout Indonesia. The primary elections have been held in 1998.

Since then, Indonesia has entered a brand new political period often known as ‘Reformasi’, marked by vital reforms to the judiciary, legislature, and government workplaces, together with the elimination of the ‘President for Life’ title and the limitation of presidential tenure to 2 5-year phrases. These reforms have been instrumental in remodeling Indonesia right into a extra democratic society, enhancing the rule of legislation, and selling political stability.

The Jokowi legacy: stability and development

Quick ahead to the presidency of Joko Widodo (popularly often known as Jokowi), the well-loved, outgoing president whose approval score had remained above 60% for probably the most a part of his 10-year tenure1. President Jokowi linked with the youthful inhabitants by way of social media and impressed many younger Indonesians together with his story of rising from a humble background to changing into the nation’s chief by way of hard-work. His administration delivered robust financial growth and job development, ensured strong authorities funds management, and furthered reforms to the state equipment to extend effectivity and scale back corruption. The Jokowi authorities is thought to be probably the most secure in trendy Indonesian political historical past.

2024 presidential election and the brand new administration

The 2024 presidential elections concluded easily in February, with just one spherical of voting. The elected pair, President Prabowo and Vice President Gibran (Jokowi’s eldest son), are seen as a continuation of the Jokowi platform. That is evidenced by Prabowo’s dedication to persevering with Jokowi’s reforms, together with increasing commodities downstream processing, constructing infrastructure, and shifting the capital to Nusantara.

A balancing act: populist insurance policies and monetary self-discipline

Nevertheless, this incoming administration leans in the direction of populist insurance policies, which is able to possible improve the federal government fiscal deficit from 1.7% to the three% statutory restrict, pushing authorities debt-to-GDP from the present 40% nearer to 50%2. Prabowo’s marketing campaign insurance policies embody free lunch plans for each pupil, increased spending on infrastructure and ramping up defence capabilities. Prabowo has urged that the elevated deficit will possible be funded by increased tax assortment from improved automated tax techniques and numerous tax reforms, together with the elimination of tax incentive packages. Nevertheless, the feasibility of this method stays in query: Indonesia’s tax system is guide and cumbersome, leading to a comparatively low tax-to-GDP ratio of 12.1%, in comparison with the typical of 19.3% in different rising Asian nations3.

Market sentiment: navigating investor considerations

Prabowo’s proposed insurance policies have triggered consternation amongst a few of Jokowi’s current cupboard ministers, in addition to international monetary market contributors. Because the election, Indonesian authorities bonds have underperformed their Asian friends. Numerous bulletins, together with the appointment of Prabowo’s nephew, Thomas Djiwandono, as second deputy finance minister, have added to traders’ considerations a few attainable improve in bond provide.

Regardless of considerations round increased public debt ranges, we imagine the market response is overdone. Even at a 50% debt-to-GDP ratio, Indonesia’s debt stage remains to be considerably decrease than different Southeast Asian economies: 66% for Malaysia, 58% for the Philippines, and 61% for Thailand4. Indonesia is unlikely to be downgraded by score businesses because the debt-to-GDP stage stays throughout the vary for Baa/BBB-rated sovereigns.

Deutsche Financial institution estimates that if the deficit-to-GDP ratio will increase from low 2% to three%, even with out development in authorities income assortment, the debt-to-GDP ratio is unlikely to exceed 50%5. The federal government also can utilise its USD 30 billion money stability, at the moment 3 times increased than pre-COVID ranges, to fund the rise in future spending, thus decreasing reliance on further authorities bond issuance. The Indonesian authorities can subsequently afford to run a better funds deficit; nevertheless, this should crucially include larger management to stop the corruption that has run rampant all through its political historical past.

Infrastructure funding: bridging the hole

Indonesia has maintained tight management over its authorities funds for many years, resulting in underinvestment within the infrastructure wanted for the nation’s development (determine 1).

Whereas Jokowi’s infrastructure drive has helped Indonesia meet up with the remainder of Southeast Asia, a lot work stays to enhance connectivity throughout the nation’s seventeen thousand islands. Prabowo’s deliberate infrastructure push is critical to proceed diversifying away from commodity exports by enhancing infrastructure for sectors together with manufacturing, processed commodities, transport, sustainable power, and tourism. Improved infrastructure will likely be key to draw overseas funding and enhance industrial productiveness.

Future prospects

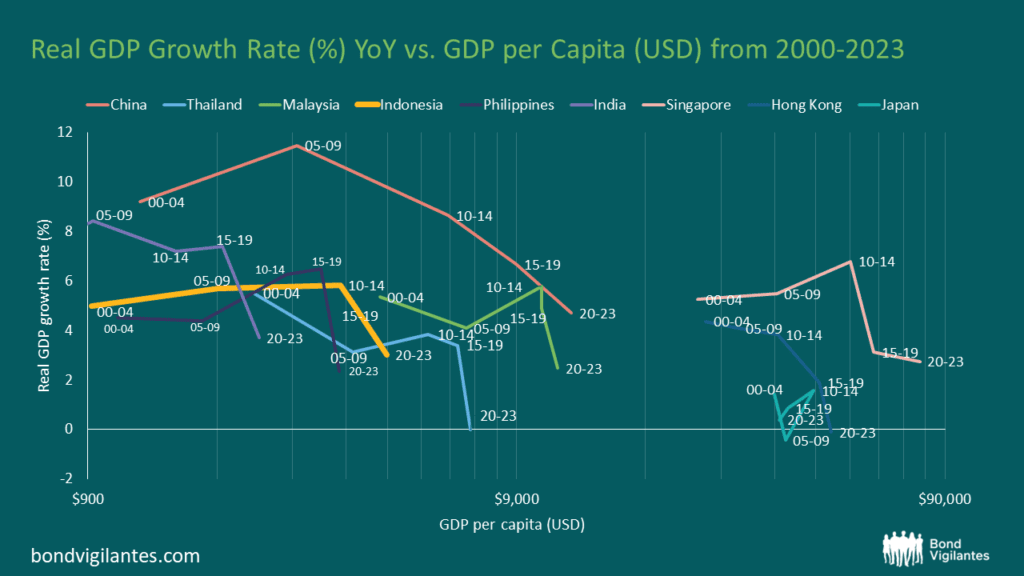

Indonesia is at a crucial juncture in its financial growth. With a comparatively younger and more and more educated inhabitants, the nation has a conducive backdrop for productiveness development. Prabowo’s GDP development goal of 8% aligns with what is required for the nation to keep away from the ‘Center Revenue Entice’ (determine 2) and obtain high-income standing earlier than the inhabitants begins getting old.

Indonesia has posted robust GDP development of over 5% for the final three many years, besides through the Asian Monetary Disaster and the COVID-19 pandemic. Nevertheless, the speed nonetheless undershoots its development potential of 7-8%. At the moment Indonesia is a lower-middle earnings economic system with GDP-per-capita of USD 4,788 in 20226. Reaching high-income standing would require coordinated efforts from each the private and non-private sectors to increase financial developments.

Investor outlook

We are going to proceed to observe Indonesia intently over the approaching months as particulars of financial insurance policies and incoming ministerial appointments are finalised. International traders will stay cautious about any departure which is perceived to be a step away from the course of Jokowi’s administration. In the meantime, Financial institution Indonesia (BI) and US financial coverage will stay the important thing drivers of home bond market efficiency. BI’s means to comply with the tempo of US charge cuts will depend on the steadiness of the Indonesian rupiah. The issuance of brief time period notes (Financial institution Indonesia Rupiah Securities or SRBI) at 7.0 – 7.5% for a 12-month tenor has improved the speed of return on the rupiah. If this proves efficient in stabilising the forex and with overseas traders’ participation in Indonesian authorities bonds at an all-time low, we imagine the circumstances are enhancing for Indonesian bonds to hitch a worldwide rally led by charge lower expectations.

1 Supply: M&G Investments estimates, primarily based on numerous media reviews, July 2024

2 Supply: Deutsche Financial institution estimates, June 2024

3 Supply: OECD, Income Statistics in Asia and the Pacific, 2022

4 Supply: IMF, Bloomberg, 2022

5 Supply: Deutsche Financial institution estimates, June 2024

6 Supply: World Financial institution nationwide accounts knowledge, and OECD Nationwide Accounts knowledge recordsdata, 2022