https://bondvigilantes.com/wp-content/uploads/2024/09/1-feds-easing-era-1024×576.jpg

It’s typically stated that the primary reduce is the deepest, and that might be the case for the US Federal Reserve (Fed) delivering a blockbusting 50 foundation level (bp) reduce. After 918 days, this marks the tip of the financial coverage tightening introduced in to tame the “transitory” inflation that got here to a thunderous crescendo in 2022.

Markets knew a reduce was coming; it was only a query of how a lot. Predictions had been evenly cut up between a 25bp reduce and a 50bp reduce, with these favouring the latter arguing that weaker information prints wanted to be addressed, and that the Fed wanted to get forward of the curve.

There have been, after all, those that felt 25bps could possibly be extra commensurate with the financial information being quickly launched. The identical folks additionally identified {that a} reduce of half a proportion level is normally reserved for intervals of serious market occasions or throughout a recession – neither of that are staring us within the face. In the long run, nevertheless, there was little or no purpose to keep up present charges and completely no rational argument for a rise.

On this weblog, I’ll spotlight what an easing cycle from the Fed may imply for one of many asset lessons that stands to learn probably the most: rising market debt (EMD).

The reduce to set rising market debt free

The under is a reasonably easy, however efficient, chart. The gray bars illustrate the hole between the Fed’s first reduce and their subsequent hike. The inexperienced line tracks the return of the exhausting foreign money sovereign index. What we will clearly see is that the Fed’s reducing cycle serves as a powerful tailwind for riskier market segments like EMD.

There are, after all, different elements of EMD that aren’t captured on this chart, resembling exhausting foreign money corporates and native foreign money sovereigns, as their respective observe data aren’t as in depth. Nevertheless, we do observe the identical sample: US charges falling is nice information throughout the board for EMD.

That isn’t to say that every of those asset lessons strikes in keeping with each other. We might count on native foreign money sovereign bonds to carry out the strongest initially in such a situation, and we’ve already had a style of this in latest months, the place they’ve been the most important beneficiaries, in efficiency phrases, of markets changing into extra snug with the course of journey from the Fed.

A driver of that is that native foreign money bond returns profit from each rate of interest and foreign money actions. When the Fed begins reducing charges, rising markets typically comply with go well with, and decrease US charges normally weaken the greenback towards sure rising market currencies.

There are different components at play, after all, with bonds very hardly ever providing an evidence that comes solely at face worth. Decrease borrowing prices and the decrease yields of developed markets that accompany decrease coverage charges ought to encourage buyers to return to an asset class that has borne the brunt of a better price setting.

There are, after all, nonetheless potential obstacles to handle. For EMD to rally, and proceed on a constructive trajectory, we would wish a model of the US comfortable touchdown that markets have been speaking about for the previous couple of years. To be bullish on any dangerous asset class, this situation would wish to play out, and there’s loads of proof to assist this. The loosening of economic circumstances will likely be a cloth think about avoiding a extra severe downturn.

Muddying the waters is the US election going down in November, with the potential for a Trump victory set to weigh on sentiment till the result’s introduced. Whereas polls are steering in direction of a Democratic victory, we have now seen earlier than (2016, anybody?) how materially mistaken they are often.

A Harris victory could be, arguably, much less inflationary which, after all, helps easing financial coverage. Alongside a Fed now within the throes of engineering a comfortable touchdown, this might be much more supportive of the asset class.

What may be anticipated shifting ahead?

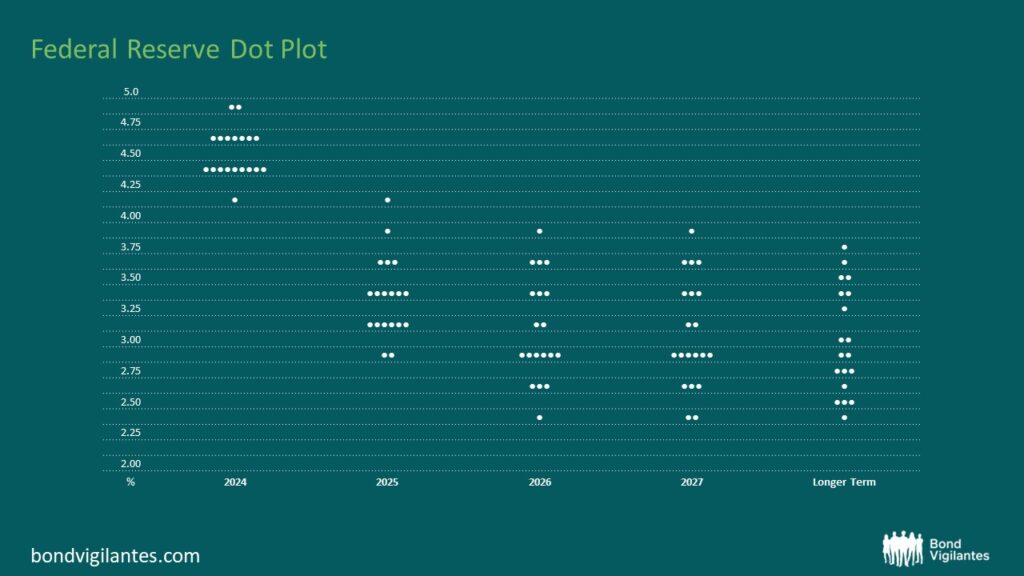

As already alluded to, EMD tends to ebb and movement in tandem with the well being of the US financial system and the present setting. With charges now falling, questions come up about what we should always count on over the subsequent few years. The under chart means that one factor we will actually rely on is uncertainty.

The dot plot itself highlights the place 16 Fed officers see coverage charges going over the subsequent few years. A quite simple however correct takeaway from the chart above is that the group is actually combined. In 2026, one member expects charges to be 2.375%, whereas one other expects 3.875%. Over the “longer-term”, we will see that there are 11 completely totally different predictions.

Nevertheless, regardless of policymakers and markets extra broadly being combined of their expectations, the course of journey now appears not open for debate, which solely strengthens the argument highlighted right here.