The Wall Road Journal revealed a bit on the inverted yield curve as a recession indicator1 just a few weeks again, mulling over why this dependable indicator appeared to be damaged. The piece is superb and is definitely worth the learn, not least as a result of they’ve blown their internet price range on dynamic graphs. To resolve the thriller, it’s useful to revisit the life and works of the Canadian asset allocation guru, Campbell Harvey.

In Could 1986, the younger Canadian was nonetheless a pupil on the College of Chicago, and campuses have been in a frenzy on the launch of the unique High Gun movie starring Tom Cruise as ‘Maverick’. Within the opening scene, Maverick and Goose stun the world with their the wrong way up aerial acrobatics resulting in a comical debriefing scene with Kelly McGillis the place Cruise utters the road, “I used to be inverted”. Although I’ve no proof that Maverick had an affect on a younger Harvey, it’s hanging to find that seven months later, he revealed his seminal dissertation which proposed that inverted yield curves (the place long run rates of interest are decrease than their shorter-dated counterparts) are harbingers of recession. Even when Maverick doesn’t seem within the dissertation footnotes (he doesn’t; I checked), Harvey’s inversion is definitely extra harmful than Maverick’s. Although Maverick can nonetheless fly all these years later, Harvey’s idea might should be grounded.

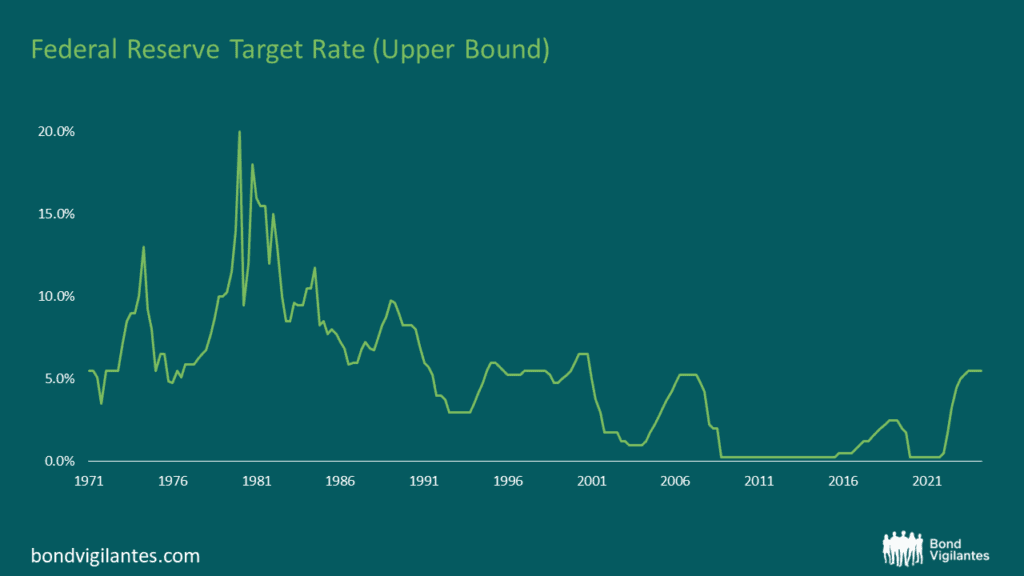

To elucidate why, first we’d like some context. The paper was revealed in December 1986 and had a revision two years later2, with the underlying information referring to the US treasury yields contemplating the years from 1900 by to 1984. Harvey famous in his introduction that the predictive energy of the indicator improved within the final 20 years of his pattern interval (1964-1984). That is vital because it clearly responded to the ‘Cease-Go’ financial coverage of the Miller and Volcker-era Federal Reserve. This was a interval when charges have been on common larger than they’re now, and little was recognized about what the Fed was going to do subsequent as this was the period previous to ahead steering.

Between 1986 and right this moment, there was a renaissance in understanding client behaviour. That is vital in its personal proper as Harvey used modern client behaviour idea to elucidate future buying selections. This kind of behavioural idea was the norm in 1986 when shoppers have been assumed to be rational and, for instance, their consumption patterns have been assumed so as to add as much as zero (that means that revenue should equate to whole expenditure). For the economists within the room, Harvey was utilizing so-called “Homo Economicus” as his client within the mannequin, signifying a Ricardian Vice (which claims {that a} mathematical system can clear up an primarily human drawback). This fashion of client idea was synonymous with the College of Chicago, the place he was writing. Kahneman & Tversky had not but come into vogue with their influential papers on Behavioural Economics

3, and so this was the accepted norm when it comes to consumption capabilities for financial papers. Right this moment, we all know that client habits and consumption patterns have advanced and so they undoubtedly don’t sum to zero because it was as soon as assumed (suppose: buy-now-pay-later platforms), and preferences are extra dynamic than they have been as soon as regarded as. These new patterns of behaviour have been formed as the worldwide economic system advanced by the Nice Moderation as much as the World Monetary Disaster in 2007, and as much as the current. This brings Harvey’s paper into query as he goes to nice lengths to impute client behaviour into his methodology to determine causes for yield unfold variations.

Crucially, the paper pre-dates the ahead steering of Alan Greenspan on the Federal Reserve (2/2/2000) which is vital on this occasion. In 2000, Chairman Greenspan started to commonly embrace a type of ahead steering within the type of the ‘Evaluation of the Stability of Dangers Going through the Economic system’ inside the Fed’s press releases. By deploying ahead steering, financial coverage makers in impact tied down an excessive amount of of the yield curve, thus limiting its capacity to invert. By switching from free market forces to the central bankers trying to regulate the curve, we find yourself with a a lot smaller group of people in charge of the knowledge that’s represented by the yield unfold. By means of time, this place has additionally change into the norm because the Financial institution of England4 and the Financial institution of Japan5 have adopted go well with. This was not the case in 1986, and so was not captured within the information that Harvey utilized in his paper. Because the publication of Harvey’s analysis, now we have had a complete rethinking of client behaviour in addition to a reshaping of Federal Reserve coverage which lowered the variety of variables that the yield unfold has to take note of. Because of this, this can be a purpose why we haven’t seen a US recession but: the correlation between the 2 could also be damaged, main us to see the longest inversion interval in current historical past. Though this doesn’t imply the indicator doesn’t work anymore, it could merely signify that it takes longer for the impact to happen. Discerning Bond Vigilantes readers will recall Andrew Eve’s 2023 Halloween piece6 highlighting that it’s not the inversion that’s the concern, it’s the steepness of the yield curve that you must fret over. To this finish, now we have seen a gentle reversion of yields over the previous few months to a extra subdued stage, which means that the anticipated recession has bugged out (as Maverick may say).

Between 1986 and the arrival of Greenspan, the idea has labored fantastic and has certainly predicted a number of recessions with accuracy. The argument right here is that, given the size of time that has lapsed because the yield curve’s most up-to-date inversion, plus the evolution of modifications to central financial institution coverage and client idea, the inversion indicator isn’t as correct because it as soon as was, and may subsequently be handled with warning.

It’s both that or we actually ought to all be singing “Freeway to the Hazard Zone”…

2 https://folks.duke.edu/~charvey/Analysis/Published_Papers/P1_The_real_term.pdf

4 https://www.bankofengland.co.uk/-/media/boe/information/speech/2013/forward-guidance-and-its-effects

5 https://www.boj.or.jp/en/mopo/mpmsche_minu/minu_1999/g990409.htm

6 Six scary charts – completely happy Halloween! – Bond Vigilantes